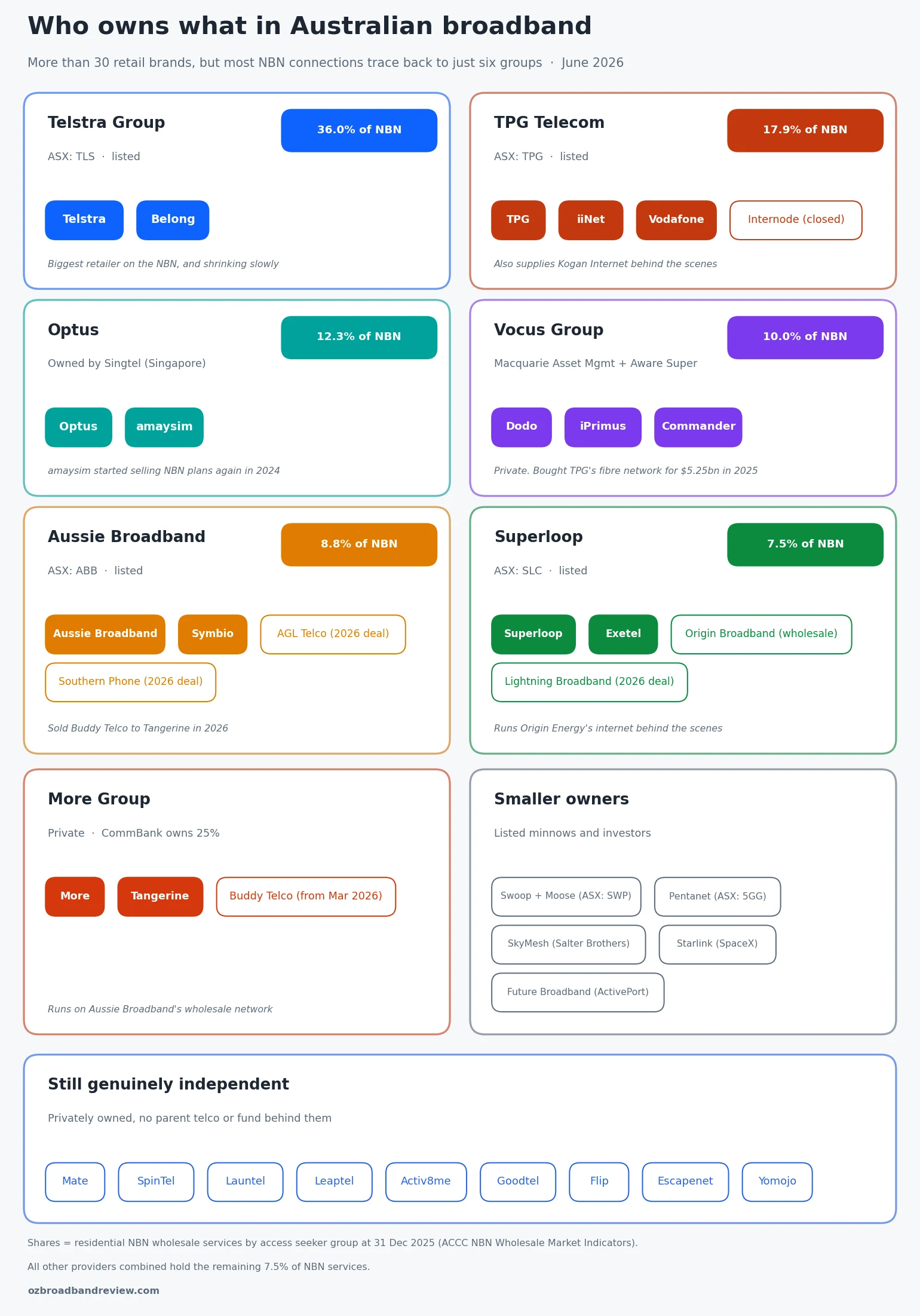

Australia looks like it has a crowded internet market. Count the brands on any plan comparison table and you’ll get past 30 without trying. Follow the ownership paperwork, though, and most of those brands lead back to just six companies. At the end of December 2025 those six groups supplied 92.5% of the 8.8 million NBN connections in the country (ACCC NBN Wholesale Market Indicators, December 2025 quarter). You think you’re choosing between 30 providers. Mostly, you’re choosing between six owners.

This post maps who owns what in Australian broadband as of June 2026, and how much money each parent company makes. Everything here comes from public documents: ASX results, annual reports, company announcements and the ACCC’s quarterly market data. The references are all listed at the bottom so you can check any number yourself.

Why are there so few owners?

Two decades of takeovers. TPG and Vodafone merged in 2020. Vocus was taken private by Macquarie Asset Management and Aware Super in 2021, the same year Superloop bought Exetel for $110 million and Optus bought amaysim. Aussie Broadband picked up Over the Wire in 2022 and Symbio in 2023. And the deals haven’t slowed down. In July 2025 Vocus completed a $5.25 billion purchase of TPG’s entire fibre network. In February 2026 Aussie Broadband announced it was buying AGL’s telco business, including Southern Phone, while Superloop announced a $165 million deal for Lightning Broadband’s parent company. Even Buddy Telco, launched by Aussie Broadband in 2024, was sold to Tangerine with customer migration starting in March 2026.

Here’s each owner group in order of size, with the brands they control and the money they make.

Telstra Group: Telstra and Belong

Telstra (ASX: TLS) is still the biggest internet retailer in Australia by a wide margin, with 36.0% of all NBN services at December 2025 (ACCC). Its only other fixed broadband brand is Belong, the budget label it launched in 2013. The money is enormous: total income of $23.6 billion and a profit of $2.2 billion in the year to June 2025 (Telstra FY25 results). Telstra’s consumer fixed business had about 3.2 million bundle and data services at June 2025, and the average Telstra fixed customer was paying $87.08 a month, the highest average in the market.

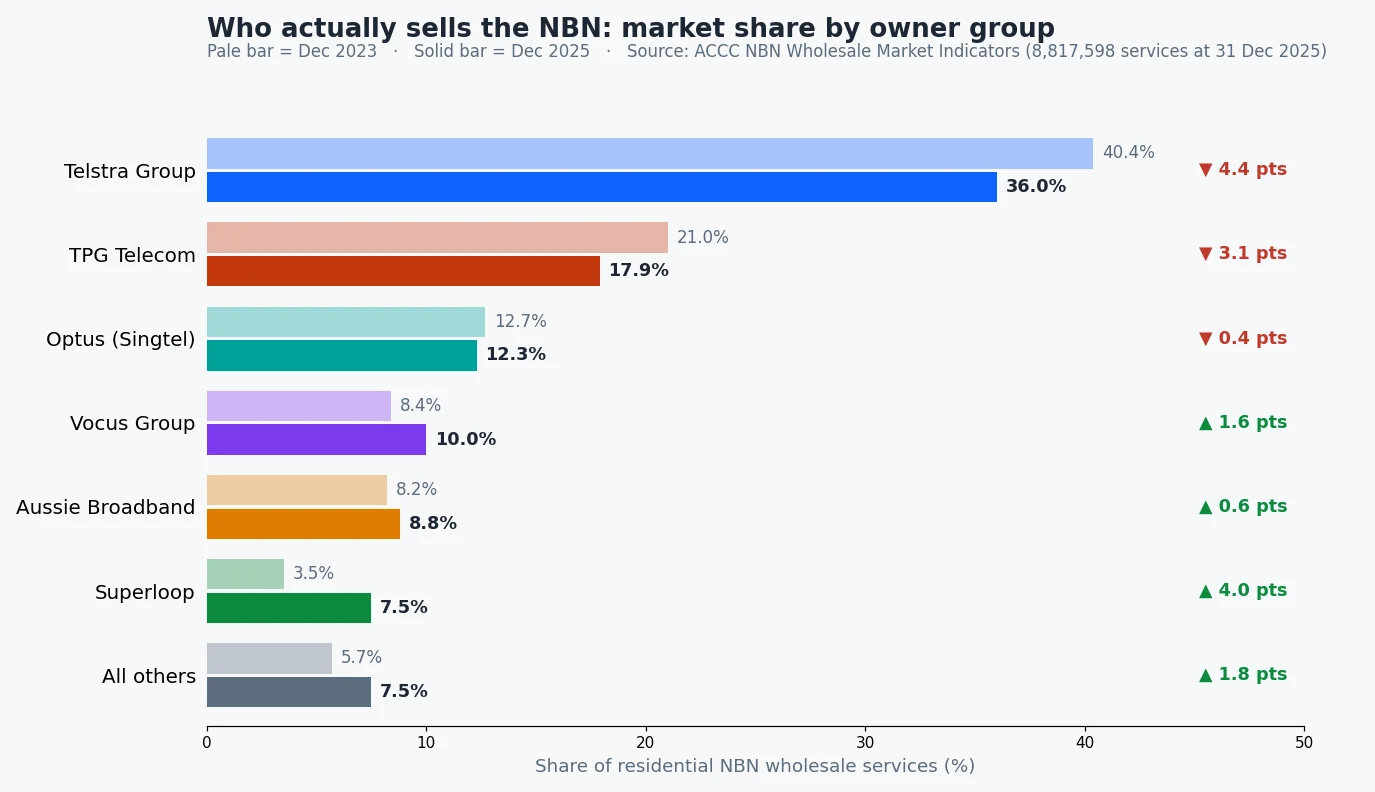

The interesting part is the direction. Telstra’s share of the NBN was 40.4% two years earlier. It has shed services every single quarter in the ACCC dataset since, around 364,000 services over two years, mostly to the challengers further down this list.

TPG Telecom: TPG, iiNet, Vodafone and the ghost of Internode

TPG Telecom (ASX: TPG) owns TPG, iiNet and Vodafone, plus the mobile brands felix and Lebara. Internode, the much loved Adelaide ISP, was closed to new customers in December 2023 and its base migrated to iiNet. TPG also supplies Kogan Internet behind the scenes; Kogan is a white label riding on TPG’s network, not a TPG brand.

TPG reported revenue of $5.04 billion for calendar 2025, with 1,568,000 NBN subscribers paying an average of $74.37 a month (TPG FY25 results, February 2026). The headline event was the sale of its fibre network, enterprise business and Vision Network to Vocus for $5.25 billion, completed 30 July 2025. TPG kept the consumer brands and the mobile network; the infrastructure underneath went to Vocus. The sale also made the profit line look better than the business underneath it: reported profit was $461 million, but $409 million of that came with the sold assets, leaving $52 million from ongoing operations.

Read enough Whirlpool threads about iiNet and a pattern emerges: people who signed up in the 2000s for the famous support eventually realise the company behind the brand has changed twice while their direct debit stayed the same. The brand on the bill and the company answering the phone are not the same thing, and that’s really the point of this whole post.

Optus: Optus and amaysim, owned in Singapore

Optus is wholly owned by Singtel, the Singaporean telco giant. Its second brand is amaysim, bought in 2021, which started selling NBN plans again in September 2024. Optus made $8.35 billion in revenue in the year to March 2026, of which $1.07 billion came from NBN broadband, from 1,069,000 NBN customers paying an average of $78 a month, with an operating profit (EBIT) of $550 million (Singtel FY26 results, May 2026). Its 12.3% NBN share has drifted down only slightly over two years, making it the steadiest of the big three.

Vocus: the biggest provider you’ve never heard of

Vocus doesn’t sell anything under its own name to households, but it owns Dodo, iPrimus and the small business brand Commander, which together held 881,243 NBN services (10.0%) at December 2025. Vocus itself is private, owned by Macquarie Asset Management and Aware Super, so it publishes no results announcements and we can’t tell you its profit. What we can tell you is that it now owns more than 50,000 km of fibre after swallowing TPG’s network in 2025, which makes the owner of Dodo one of the biggest infrastructure players in the country. Its NBN share is growing too, up from 8.4% two years ago.

Aussie Broadband: the challenger that became an aggregator

Aussie Broadband (ASX: ABB) made $1.19 billion in revenue in the year to June 2025, up 18.7%, with a profit of $32.8 million and 788,400 broadband connections on its network (ABB FY25 results). By December 2025 that was 827,700 connections and an 8.8% NBN share.

Its ownership story is busy. It bought the wholesale voice provider Symbio in 2023. It launched Buddy Telco as its own budget brand in 2024, then sold it to Tangerine in 2026. And in February 2026 it announced the purchase of AGL’s telco arm, including Southern Phone, for $115 million in shares: about 350,000 broadband and mobile services plus 46,000 voice services, with AGL taking a stake of around 7.5% in Aussie Broadband and continuing to market telco under the AGL brand. Aussie Broadband says the deal will make it the third largest NBN provider by the end of 2026. On top of the brands it owns, it also runs the network underneath More and Tangerine (more on them below).

Superloop: Exetel, plus Origin Energy’s internet behind the scenes

Superloop (ASX: SLC) owns Exetel, which it bought for $110 million in 2021. It also has the most interesting wholesale deal in the market: since October 2024 every Origin Broadband customer has actually been on Superloop’s network, under an exclusive six year agreement. Origin passed 250,000 broadband subscribers in March 2026, and none of them are really with an energy company at all.

Superloop is the fastest grower of the six. Its NBN share went from 3.5% to 7.5% in two years, and revenue hit $546.5 million in the year to June 2025, up 31%, with its first ever profit of $1.2 million (Superloop FY25 results). In February 2026 it announced a $165 million deal to buy Lynham Networks, the company behind Lightning Broadband. It also absorbed MyRepublic’s roughly 52,000 Australian customers when that provider left the market at the end of 2022.

The More group: the quiet fourth force, part owned by CommBank

More and Tangerine are privately owned sister companies, founded in Melbourne in 2013 by brothers Andrew and Richard Branson (no relation to the Virgin one). The Commonwealth Bank bought a 25% stake in both in 2021, which is why CommBank app users get offered discounted NBN. Aussie Broadband puts their combined base at roughly 250,000 customers, all moving onto Aussie Broadband’s wholesale network through 2026 under a six year agreement. Add Buddy Telco, which Tangerine bought from Aussie Broadband with migration starting March 2026, and the group is past 270,000 services. Your bank now has a meaningful seat in your internet market.

Who actually sells the NBN: the numbers

| Owner group | NBN services (Dec 2025) | Share | Share two years earlier |

|---|---|---|---|

| Telstra Group | 3,177,603 | 36.0% | 40.4% |

| TPG Telecom | 1,578,501 | 17.9% | 21.0% |

| Optus (Singtel) | 1,084,381 | 12.3% | 12.7% |

| Vocus Group | 881,243 | 10.0% | 8.4% |

| Aussie Broadband | 773,025 | 8.8% | 8.2% |

| Superloop | 657,681 | 7.5% | 3.5% |

| All other providers | 665,164 | 7.5% | 5.7% |

Residential NBN wholesale services by access seeker group at 31 December 2025, total 8,817,598 services (ACCC NBN Wholesale Market Indicators, published March 2026). Percentages are calculated from the ACCC’s service counts. One caveat: smaller providers often buy NBN access through aggregators, so the true retail share of the “all others” group is a bit higher than 7.5%.

How much money do they make?

| Owner | Ownership | Latest annual revenue | Profit | Reporting period |

|---|---|---|---|---|

| Telstra Group | Listed (ASX: TLS) | $23.6 billion total income | $2.2 billion profit | Year to June 2025 |

| Optus | Singtel (Singapore) | $8.35 billion | $550 million EBIT | Year to March 2026 |

| TPG Telecom | Listed (ASX: TPG) | $5.04 billion | $52 million profit (ongoing business) | Calendar 2025 |

| NBN Co (the network) | Australian Government | $5.7 billion | $1.2 billion loss | Year to June 2025 |

| Vocus Group | Private (Macquarie AM + Aware Super) | Not published | Not published | n/a |

| Aussie Broadband | Listed (ASX: ABB) | $1.19 billion | $32.8 million profit | Year to June 2025 |

| Superloop | Listed (ASX: SLC) | $546.5 million | $1.2 million profit | Year to June 2025 |

| More group (More, Tangerine, Buddy) | Private, CBA 25% | Not published | Not published | n/a |

| Swoop (incl. Moose) | Listed (ASX: SWP) | $106.5 million | $6.9 million loss | Year to June 2025 |

Three notes on the profit column. Profit means net profit after tax as each company reported it. Optus is the odd one out because it only publishes operating profit (EBIT), which is measured before interest and tax, so it isn’t directly comparable to the others. And TPG’s reported 2025 profit was actually $461 million, but $409 million of that came with the businesses it sold to Vocus; $52 million is what the ongoing operation made. The thin margins outside the big two are real: Superloop turned its first ever profit in 2025 and Swoop is still loss making once depreciation is counted.

A number worth sitting with: NBN Co itself, the government owned company that runs the actual network, made $5.7 billion in revenue in the year to June 2025 with 8.63 million premises connected and an average wholesale charge of $50 a month per home (NBN Co FY25 results). And yet NBN Co still booked a $1.2 billion loss in FY25 once depreciation and the interest on building the network were counted (NBN Co FY25 financial report). Roughly two thirds of your monthly bill goes straight through your provider to NBN Co. Whoever you pick at the retail level, the biggest slice of the money ends up in the same place.

Who is still genuinely independent?

A shrinking but real club. Mate is still owned by its Sydney founders, twins David and Mark Fazio and Jonathan Dundovic. SpinTel has been privately owned since 1996. Leaptel is Melbourne owned, Launtel is Launceston owned, Activ8me is the trading name of Australian Private Networks, and Goodtel is a B Corp that donates half its profits. Flip and Escapenet are private too, though Flip’s customers ride on Swoop’s network under a wholesale deal.

Then there are the small fry with their own owners: Swoop (ASX listed, owns Moose), Pentanet (Perth, ASX listed), Future Broadband (owned by ASX listed ActivePort), SkyMesh (bought by investment manager Salter Brothers in December 2024 for up to $50 million) and Starlink, which is SpaceX, about as foreign owned as it gets.

Does it matter who owns your provider?

More than you’d think, and less than the brands would like. Less, because the physical network is the same: NBN Co owns the wires regardless of whose logo is on your bill, so the maximum speed at your address doesn’t change when ownership does. More, because ownership decides nearly everything else: where the support call centre is, how much bandwidth the provider buys to cover the evening peak, how quickly prices move after NBN Co changes its wholesale charges, and whether the brand you joined still operates the way it did when you joined it.

It also means “switching” between two brands of the same parent is barely switching. Move from Dodo to iPrimus and you’ve changed the logo, not the company. Move from TPG to iiNet, same. If you’re leaving because of support quality or congestion, check this map first; the fix is usually moving to a different owner group, not a different brand. Our own review data backs this up: in our reliability rankings and support rankings, the gaps between owner groups are much bigger than the gaps between brands of the same group.

What this means for you

The consolidation isn’t automatically bad. Aussie Broadband and Superloop got big by being better than the incumbents, and the ACCC numbers show Australians rewarding them for it, one switch at a time. But it does mean the market is more concentrated than the shelf suggests, and that the cheapest brands are increasingly just discount labels for the companies above them. If you’re shopping on price, that’s fine, but know whose network and support queue you’re actually buying.

If this post has you eyeing a switch to one of the challengers, these are the cheapest NBN plans from our partner providers right now:

|

Value

25 Mb/s

Unlimited data

|

$47.9/mth

for 6 mths,

then $72.9/mth |

Go to site |

|

Basic - nbn 12/1

12 Mb/s

Unlimited data

|

$77/mth | Go to site |

|

Everyday

25 Mb/s

Unlimited data

|

$58/mth

for 6 mths,

then $78/mth |

Go to site |

|

One Plan

500 Mb/s

Unlimited data

|

$80/mth | Go to site |

|

Value

25 Mb/s

Unlimited data

|

$80/mth | Go to site |

| Click here to view more NBN plans | |||

A quick disclosure: some providers pay us a commission if you join through our links. That has no bearing on anything in this post; every ownership fact and dollar figure above comes from public records, and the full list is below. If you want to see how real customers rate the brands in this map, start with our most recommended providers rankings, or read up on how to switch without downtime.

Frequently asked questions

Who owns iiNet?

iiNet is owned by TPG Telecom, the ASX listed company formed when TPG and Vodafone Hutchison Australia merged in 2020. iiNet has not been independent since 2015, when TPG bought it for $1.56 billion. TPG also owns the TPG and Vodafone brands, and it closed Internode to new customers in December 2023, migrating those customers to iiNet.

Who owns Dodo?

Dodo is owned by Vocus Group, along with iPrimus and the small business brand Commander. Vocus is a private company owned by Macquarie Asset Management and Aware Super. Vocus also bought TPG’s entire fibre network for $5.25 billion in July 2025, so Dodo’s parent is one of the biggest fibre owners in Australia.

Is Belong owned by Telstra?

Yes. Belong is Telstra’s budget brand and has been since Telstra launched it in 2013. Belong customers are on the Telstra group’s NBN arrangements, and the ACCC counts Belong’s services inside Telstra’s 36.0% market share. It’s a separate brand with separate plans and support, but the money flows to the same company.

Who owns Tangerine and More?

More and Tangerine are privately owned sister companies founded in Melbourne in 2013 by brothers Andrew and Richard Branson (not the Virgin founder). The Commonwealth Bank owns a 25% stake in both, taken in 2021. Tangerine also bought the Buddy Telco brand from Aussie Broadband in 2026. The group’s customers run on Aussie Broadband’s wholesale network.

Does Origin Energy run its own broadband network?

No. Origin Broadband is sold by Origin Energy, but since October 2024 the service has run entirely on Superloop’s network under an exclusive six year wholesale agreement. Origin passed 250,000 broadband subscribers in March 2026. If you have a problem with an Origin connection, the network being fixed is Superloop’s.

Are amaysim and Optus the same company?

Yes. Optus bought amaysim in 2021, and Singtel of Singapore owns Optus outright. amaysim returned to selling NBN plans in September 2024 after years as a mobile only brand. The ACCC counts amaysim services inside the Optus group’s 12.3% share of the NBN market.

Who is the biggest NBN provider in Australia?

Telstra, with 3,177,603 residential NBN services at 31 December 2025, which is 36.0% of the market (ACCC NBN Wholesale Market Indicators). That counts Belong too. TPG Telecom is second at 17.9% and Optus third at 12.3%. Telstra’s share is falling though; it was 40.4% two years earlier.

Who owns the NBN itself?

The Australian Government. NBN Co is a government business enterprise owned by the Commonwealth, and every retail provider in this post pays it wholesale charges to use the network. NBN Co made $5.7 billion in revenue in the year to June 2025, with 8.63 million homes and businesses connected.

Which NBN providers are still independent?

Mate, SpinTel, Launtel, Leaptel, Activ8me, Goodtel, Flip and Escapenet are all still privately owned with no parent telco or investment fund behind them. Swoop and Pentanet are independent too but listed on the ASX. Between them, providers outside the big six groups hold about 7.5% of NBN services.

References

Every figure in this post comes from one of these public documents, all current as of June 2026:

- ACCC, NBN Wholesale Market Indicators Report, December quarter 2025 (published 23 March 2026)

- Telstra, financial results for the full year ended 30 June 2025 (August 2025)

- TPG Telecom, FY25 results media release (February 2026)

- Optus, FY26 financial results media release (May 2026)

- Vocus, completion of the TPG fibre and EG&W acquisition (30 July 2025)

- Aussie Broadband, FY25 results announcement (August 2025)

- Aussie Broadband, H1 FY26 investor briefing including the AGL Telco acquisition (February 2026)

- Superloop, FY25 results presentation (August 2025)

- Origin Energy and Superloop, broadband services agreement (March 2024)

- Commonwealth Bank, 25% stake in More Telecom and Tangerine (July 2021)

- NBN Co, FY25 results (August 2025)

- NBN Co, FY25 financial report (August 2025)

- Swoop Holdings, FY25 full year results announcement (August 2025)

- Salter Brothers, SkyMesh acquisition (December 2024)